38 duration for zero coupon bond

Zero Coupon Bond Modified Duration Formula | Bionic Turtle Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/(1+0.04/2) under semi-annually compounded yield of 4.0%. Duration of zero coupon bond - Fixed Income - AnalystForum 10 Oct 2007 — The weight used for each cash flow is its present value divided by the total present value of the bond. In the very simple case of a zero coupon ...

What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with ...

Duration for zero coupon bond

Bond duration - Wikipedia Macaulay duration is a time measure with units in years and really makes sense only for an instrument with fixed cash flows. For a standard bond, the Macaulay ...

Duration for zero coupon bond. Bond duration - Wikipedia Macaulay duration is a time measure with units in years and really makes sense only for an instrument with fixed cash flows. For a standard bond, the Macaulay ...

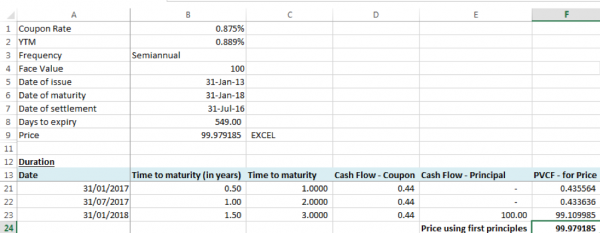

EXCEL Duration Calculation between Coupon Payments ...

YTD Top Performer Long Term Government Bond Mutual Funds 2012 | MEPB ...

6) You purchased a zero-coupon bond one year ago for $276.83. The ...

Post a Comment for "38 duration for zero coupon bond"