43 zero coupon bonds duration

What Is a Zero-Coupon Bond? Definition, Characteristics & Example For instance, if a zero-coupon bond was sold at a $100 discount and matures in four years, its holder would have to pay the applicable bond interest tax rate on $25 worth of the bond's total $100 ... › dictionary › dWhat Is Duration of a Bond? - TheStreet Definition - TheStreet Mar 22, 2022 · Zero-Coupon Bonds. The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity.

25+ Year Zero Coupon U.S. Treasury Index Exchange-Traded Fund - PIMCO The fund's ETF structure allows for trading throughout the day with the same expense ratio for all investors, regardless of investment size. Portfolio Information 22 Number of Holdings As of 06/23/2022 26.80 Years Effective Maturity As of 06/23/2022 26.60 Years Effective Duration As of 06/23/2022 3.26% est. yield to maturity As of 06/23/2022

Zero coupon bonds duration

What Is a Zero Coupon Yield Curve? (with picture) The zero coupon rate is the return, or yield, on a bond corresponding to a single cash payment at a particular time in the future. This would represent the return on an investment in a zero coupon bond with a particular time to maturity. The zero coupon yield curve shows in graphical form the rates of return on zero coupon bonds with different ... What Is Duration of a Bond? - TheStreet Definition - TheStreet 22.03.2022 · Zero-Coupon Bonds. The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. calculator.me › savings › zero-coupon-bondsZero Coupon Bond Value Calculator: Calculate Price, Yield to ... Economist Gary Shilling mentioned holders of 30-year zero-coupon bonds purchased in the early 1980s outperformed the S&P 500 with dividends reinvested by 500% over the subsequent 30-years as interest rates fell from around 14.6% to around 3%. I started investing in 30 Year zero coupon treasuries. Now, zero coupon bonds don't pay any interest ...

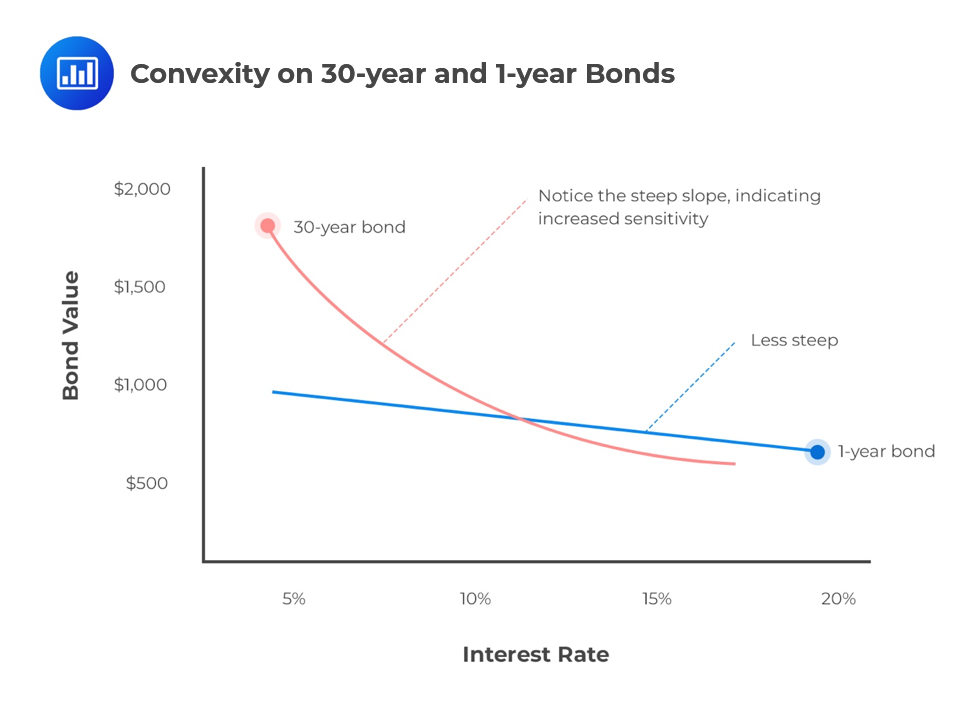

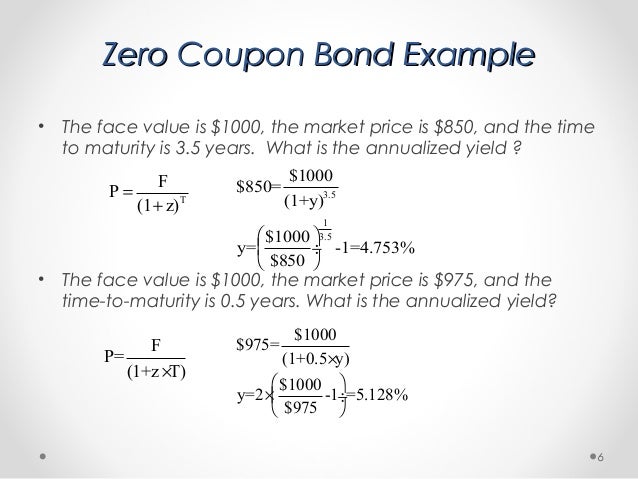

Zero coupon bonds duration. › zero-coupon-bondZero Coupon Bond (Definition, Formula, Examples, Calculations) = $463.19. Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. How to Worry about Duration - Verdad Because not only did the two-year coupon rise from 0.13% to 0.58%, but the yield curve also got dramatically steeper. The rate jump from one to two years went from 0.03% at the end of 2020 to 0.33% at the end of 2021. Now it's tempting to look at this and think, wow, it's hard to lose money on the short end, so I should just stay short. Advantages and Risks of Zero Coupon Treasury Bonds 31.01.2022 · Zero coupon bonds are bonds that do not make any interest payments until maturity, ... "Price History Search: Ext Duration Treasury ETF." Accessed July 2, 2021. PIMCO. Bond Duration - Understanding Interest Rate Risk A bond duration of 5 years would imply that the bond's price changes by 5% if yields go up or down by 100bp. In practice, bond prices do not move linearly but are convex by nature. Bond prices gain more than they fall for the same change in yields i.e., the price gain for a 100bp fall in yields is more than the price loss for a 100p rise in yields.

Duration - Definition, Types (Macaulay, Modified, Effective) It is a measure of the time required for an investor to be repaid the bond's price by the bond's total cash flows. The Macaulay duration is measured in units of time (e.g., years). The Macaulay duration for coupon-paying bonds is always lower than the bond's time to maturity. For zero-coupon bonds, the duration equals the time to maturity. Duration and Convexity, with Illustrations and Formulas Among bonds with the same YTM and term length, lower coupon bonds have a higher convexity, with zero-coupon bonds having the highest convexity. This results because lower coupons or no coupons have the highest interest rate volatility , so modified duration requires a larger convexity adjustment to reflect the higher change in price for a given change in interest … dqydj.com › zero-coupon-bond-calculatorZero Coupon Bond Calculator – What is the Market Price? - DQYDJ Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) Zero coupon bonds are particularly sensitive to interest rates, so they are also sensitive to inflation risks. Inflation both erodes the ... Zero-Coupon Bonds : What is Zero Coupon Bond? - Groww A zero-coupon bonds pays no interest and trade at a discount to its face value. Get to know its meaning, advantages, price calculation. Home > Personal Finance > Zero-Coupon Bond. ... Duration risk: Duration risk is related to the sensitivity of the bond’s price to a one percent change in the interest rate.

Coupon Bond - Guide, Examples, How Coupon Bonds Work Let's imagine that Apple Inc. issued a new four-year bond with a face value of $100 and an annual coupon rate of 5% of the bond's face value. In this case, Apple will pay $5 in annual interest to investors for every bond purchased. After four years, on the bond's maturity date, Apple will make its last coupon payment. Zero Coupon Bond Calculator - Calculator Academy where ZCBV is the zero-coupon bond value; F is the face value of the bond; r is the yield/rate; t is the time to maturity; Zero Coupon Bond Definition. A zero-coupon bond is a security that does not pay interest but trades at a discount and renders a profit at maturity when the bond is redeemed for its face value. Zero Coupon Bond Example Understanding Zero Coupon Bonds - Part One - The Balance Zero coupon bonds generally come in maturities from one to 40 years. The U.S. Treasury issues range from six months to 30 years and are the most popular ones, along with municipalities and corporations. 1 Here are some general characteristics of zero coupon bonds: Issued at deep discount and redeemed at full face value Your Money: How duration of a bond determines its degree of price risk Bond duration is a key issue of interest to bond market investors. Duration is a measure of the price risk of a bond. ... Zero coupon bonds do not pose this kind of risk because there is nothing ...

Government Bonds | Tendercapital

Basics Of Bonds - Maturity, Coupons And Yield Current yield is the bond's coupon yield divided by its market price. To calculate the current yield for a bond with a coupon yield of 4.5 percent trading at 103 ($1,030), divide 4.5 by 103 and multiply the total by 100. You get a current yield of 4.37 percent. Say you check the bond's price later and it's trading at 101 ($1,010).

What is a Zero-Coupon Bond? Definition and Meaning - Market Business News

Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Bond’s Maturity, Coupon, and Yield Level | CFA Level 1 - AnalystPrep

Bonds & Rates - WSJ Government Bonds. Loading... US Economic Calendar 6/19/22. 21-Jun 10:00 AM EDT. Existing Home Sales. Period. May. Forecast. 5.41M. Actual. 23-Jun 08:30 AM EDT. Unemployment Insurance Weekly Claims ...

The Worst Year for Bonds in History? - Compound Advisors

› articles › investingAdvantages and Risks of Zero Coupon Treasury Bonds Jan 31, 2022 · Zero-coupon bonds are also appealing for investors who wish to pass wealth on to their heirs but are concerned about income taxes or gift taxes. If a zero-coupon bond is purchased for $1,000 and ...

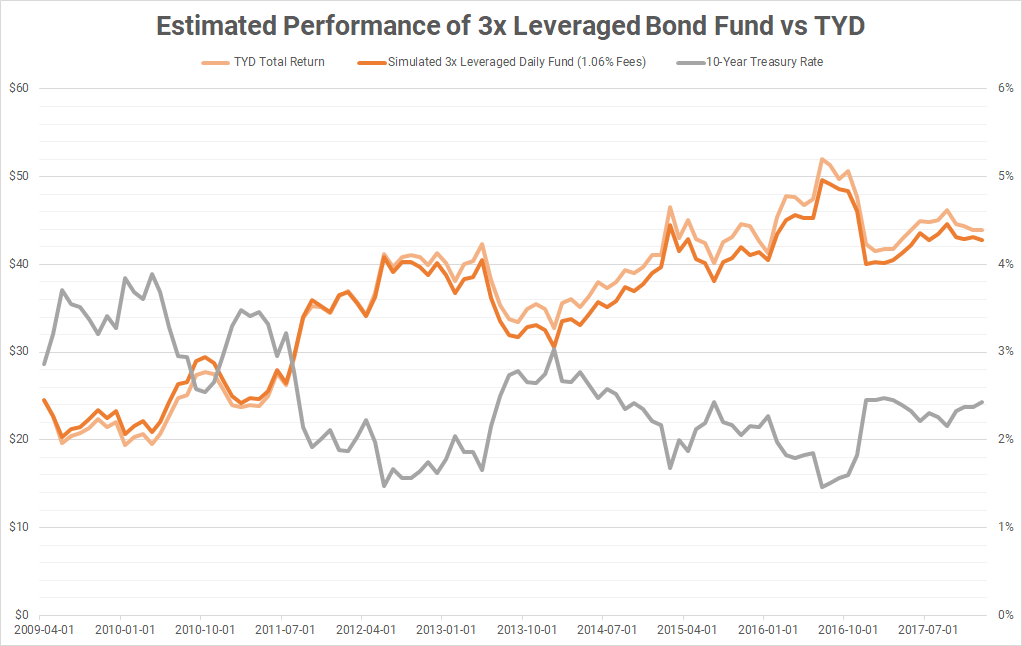

Simulated Performance Of Leveraged Bond Funds Since 1962 - Direxion ...

Dollar Duration - Overview, Bond Risks, and Formulas Dollar duration can be applied to any fixed income products, including forwarding contracts, zero-coupon bonds, etc. Therefore, it can also be used to calculate the risk associated with such products. Summary Dollar duration is the measure of the change in the price of a bond for every 100 bps (basis points) of change in interest rates.

Bonds part 1

South Africa Government Bonds - Yields Curve The South Africa 10Y Government Bond has a 10.245% yield.. 10 Years vs 2 Years bond spread is 459.5 bp. Normal Convexity in Long-Term vs Short-Term Maturities. Central Bank Rate is 4.75% (last modification in May 2022).. The South Africa credit rating is BB-, according to Standard & Poor's agency.. Current 5-Years Credit Default Swap quotation is 313.76 and implied probability of default is 5.23%.

Macaulay's Duration, a Second Look - GlynHolton.com

Zero Coupon Bond Value Calculator: Calculate Price, Yield to … Longer duration bonds are more sensitive to shifts in interest rates. And zero-coupon long duration bonds are more sensitive to rate shifts than bonds which regularly pay interest. Typically the yield curve is upward sloping with longer duration bonds offering a higher return to compensate for the added risk.

:max_bytes(150000):strip_icc()/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Coupon Rate Meaning In Hindi ~ coupon

Zero-Coupon CDs: What They Are And How They Work | Bankrate You'll receive the full face value of the CD, plus all the interest, once it matures. Let's say you buy a 5-year, $100,000 zero-coupon CD at the discounted price of $88,000. You wouldn't receive...

Post a Comment for "43 zero coupon bonds duration"